Russian legislation provides for a large number of types of commercial relations. Among these is the commission sale of non-food products.

This type of activity is regulated by separate sources of law. What are the specifics of commission trading in the Russian Federation? How are financial transactions related to it recorded in

Legislative source of rules

Let's consider the rules of commission trading in non-food products from the point of view of regulatory legislation. The main legal act that establishes them is Government Decree No. 569 of June 6, 1998. This source also correlates with the Law “On the Protection of Consumer Rights.”

Thus, commission trading is an activity that is regulated at the federal level. Let's study the structure of the basic source that defines the rules for the corresponding type of commercial activity - Resolution No. 569.

General provisions

The basic concepts approved by the legal act under consideration are “commission agent”, “committent” and “buyer”. Legislation regulates relations in which the three specified entities participate. Let us consider the essence of these terms in more detail.

A commission agent, in accordance with Government Decree No. 569, is an organization or individual entrepreneur that accepts certain goods on commission and sells them in a retail format. The principal is a person who gives the goods on commission for the subsequent purpose of sale with the participation of the commission agent and payment of remuneration to him. A buyer is a citizen who intends to buy or actually purchases goods for his own needs that are not related to entrepreneurial activities.

Commission trading is possible if both citizens of the Russian Federation and foreigners or persons who do not have citizenship in relation to any state participate in it. In relation to the principal, it is formed for products that are accepted on commission - until he sells it to the buyer. A different procedure for the exercise of property rights may be provided for by separate norms of civil legislation.

The commission agent is responsible to the principal for the preservation of consumer goods. He is also obliged to inform the principals and buyers regarding the name of his company, its address, and operating hours by placing a sign. Similarly, a person with the status of an individual entrepreneur must provide interested parties with data reflecting the fact of state registration of the company.

Reception of goods

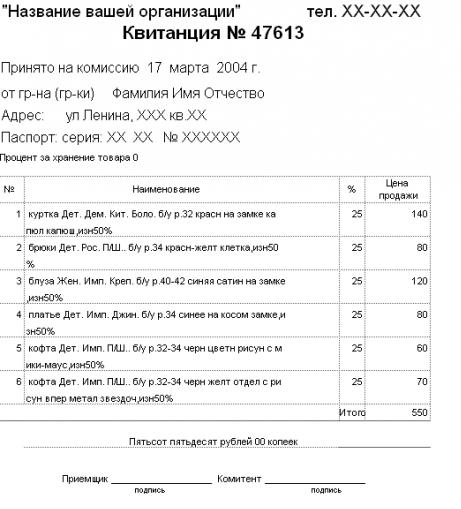

Let's consider how goods are accepted within the framework of commission communications. What should you pay attention to first? In accordance with the agreements between the commission agent and the consignor, acceptance of the goods must be carried out by drawing up a separate document. Most often this is a commission trading agreement. It can also be supplemented with invoices and other types of sources. The document in question records the date of its preparation, number, information about the parties to the transaction, the procedure for transferring the commission, its consumer characteristics and price. Also, additional clauses may be included in the structure of the source, which should not infringe on the legal rights of the committent. If several goods are transferred, a list of them is formed, which must be reflected in the contract.

Trade in vehicles

Commission trade in vehicles is carried out according to special rules. Thus, cars, motorcycles and other types of equipment that are subject to mandatory state registration can be accepted for commission only if the seller has at his disposal documents confirming ownership of them, as well as sources by which it is possible to determine the fact of removal of vehicles from accounting. The legislation of the Russian Federation also requires the issuance of temporary “transit” type signs for cars. If the vehicle is of foreign origin and its owner is in the Russian Federation temporarily, then commission trade in this case is possible only if the necessary documents issued by customs are available.

What goods are not accepted for consignment?

There are goods that cannot be accepted for commission. In general, these are all those products that are withdrawn from circulation in the Russian Federation, as well as those whose sale is limited or completely prohibited by the Russian authorities. It is impossible to sell consignment goods if they are not subject to return or exchange. You cannot sell medicines, hygiene products, perfumes and cosmetics, underwear, socks, and household chemicals. Thus, commission trade in non-food products is quite complicated due to the presence of legislative restrictions.

Registration of goods for sale

Let's look at some of the nuances regarding the correct design of a product for sale. First of all, there must be a label attached to it. If the product is small in size, then this is a price tag that records the document number related to the procedures for accepting the product for commission.

As we noted above, in some cases a separate list of items for sale may be formed. If this is so, then the label for the corresponding type of goods must include information that describes the consumer properties of the product. For example, whether it is new or, conversely, was used. The rules of commission trade in non-food products require sellers to provide reliable information about products to buyers.

Rights and obligations of transaction participants

Let us study such an aspect as the rights and obligations of the participants in the legal relations in question - the principal and the commission agent. What can you pay special attention to here? In accordance with Government Decree No. 569, the principal has the right at any time to refuse to fulfill the contract concluded with the commission agent. That is, he can cancel the order given to the partner. But at the same time, the commission agent has the right to demand compensation for losses incurred as a result of termination of the contract. The principal must, within the time limits specified in the contract, begin to dispose of his own property, which is temporarily under the jurisdiction of the commission agent. If he does not do this, then the commission agent can give the goods for storage - and the principal will pay for this service, or sell, but at a price that should be as profitable as possible for the partner.

Determining the price of the goods and the amount of the commission agent's remuneration

Perhaps the key nuance of the corresponding type of commercial relationship is determining the price of the goods that are subject to commission, as well as the amount of remuneration that the principal must pay to his partner. The rules for trading consignment goods do not include any recommendations regarding determining the price of products sold. In any case, partners will have to negotiate individually. As for the remuneration, it must in any case be paid to the commission agent. But it is quite possible that the amount of appropriate compensation is not fixed in the contract. In this case, the amount of remuneration is determined based on generally accepted indicators in a particular market segment.

How the sale is carried out

Above, we looked at what the basic requirements for goods offered for sale are: the presence of price tags and other elements that inform the buyer about the properties of the products he is purchasing. Now we can look at how the sale of goods accepted for commission is carried out in more detail. What is useful to pay attention to here?

The rules in accordance with which the commission is carried out require the relevant subjects of the commercial activities in question to launch the product for sale on the next business day after it is accepted. If this does not happen, then the principal has the right to expect a penalty from the partner. Moreover, it is decent - 3% of the amount that must be paid to the commission agent as a remuneration. In this case, the partners can agree on higher amounts of the penalty.

The commission agent is obliged to sell the goods on terms that are most beneficial to his partner. The relevant criteria can be determined by the principal himself and recorded in the contract, and if they are absent, one must be guided by the customs accepted in a particular business segment. In this case, the commission agent may deviate from the established criteria if this is in the interests of the partner, and also provided that it is not possible to agree on changes for objective reasons. However, as soon as the seller contacts the principal, he must inform him of the corresponding adjustments in the sales policy.

If a new product comes into the possession of the commission agent, and defects are discovered in it that were not noticed during the process of placing it on sale, then the corresponding product must be returned to the partner. The parties may agree on a different procedure for interaction on such issues. If the product is returned to the principal, then he does not pay any compensation to the commission agent for storing his property.

Warranty and Returns

Goods must have documents confirming it. This could be an appropriate type of coupon, registration certificate or, for example, a service book from the manufacturer. If the buyer bought a low-quality product and was not warned about its shortcomings by the commission agent, then he may demand replacement of the product with a similar one, products of a different brand (with recalculation of the price), a reduction in cost, immediate repairs, or reimbursement of costs for correcting the defects of the product.

At the same time, the law determines that the buyer also has the right to demand a refund of the money paid for the product. At the same time, of course, he must return the goods to the seller. We may well note that a citizen purchasing consignment goods has a fairly wide range of rights.

Are services sold on commission?

Is commission trading of services possible? In accordance with the Civil Code of the Russian Federation, any legal transactions can be concluded within the framework of the appropriate mechanism of legal relations. A commission agreement is possible for both goods and services.

However, when concluding such contracts, the parties to the transaction should be more guided by the provisions of the Civil Code of the Russian Federation, in particular its 51st article, and not by Resolution No. 569, which regulates only one aspect of commission relations - namely the turnover of non-food products in the appropriate format .

Accounting support

Let's look at another notable aspect that characterizes commission trading: accounting. What will interest us first? Financial settlements are an element that almost always includes commission trading. The postings must therefore be correct. Let's study their specifics.

The acceptance of goods under contracts of the corresponding type is recorded by the following entry:

- Debit 004, that is, “Goods accepted on commission.”

If it is necessary to reflect in accounting the write-off of sold products, their return or markdown, then the following entry must be recorded:

- Credit 004.

If we are talking about recording in the accounting registers the fact of receipt of cash at the cash desk as a result of the sale of accepted goods or for storage services, then the following entries must be made:

- Debit 50, that is, "Cash".

- Credit 90, that is, “Sales”, then subaccount 1 “Revenue” (reflects the amount of cash receipts for products sold).

- Credit 91, that is, “Other income and expenses” (settlements for storing goods are reflected).

The accountant also needs to charge VAT on the products sold. This must be done through the following entries:

- Debit 90, that is, “Sales”, then subaccount 3, that is, “VAT”.

- Credit 68, that is, “Calculations for taxes and fees.”

If we are talking about writing off costs, then this is recorded in the following entries:

- Credit 44, that is, “Sales Expenses”.

The transfer of funds to the principals for sold products must be reflected through the following posting:

- Debit 90, that is, “Sales”, then subaccount 2, that is, “Cost of sales”.

- Credit 76, that is, “Settlements with debtors and creditors.”

The accountant may be tasked with comparing debit and credit turnover in relation to the subaccount indicators for account 90 in order to determine the financial results from the sale of goods. How to solve it? Using the following wiring:

- Debit 90, that is, “Sales,” then subaccount 9, that is, “Profit or loss from sales.”

- Credit 99, that is, “Profit and Loss”.

In some cases, principals must receive a penalty. It is fixed in the postings:

- Debit 91, that is, “Other income and expenses.”

- Credit 50, that is, “Cashier”.

This is the specificity that characterizes commission trading. Accounting for it is carried out in accordance with standardized criteria. The corresponding commercial legal relations have a stable legislative basis. If an accountant needs to record certain financial transactions that include commission trading, the entries provided for this are quite accessible and logical.

A commission agent is usually called an enterprise that acts as an intermediary between the seller-owner of the goods and the buyer. When selling consignment items, the commission agent receives remuneration for his services; these incomes are his main source of profit.

An agreement on the provision of intermediary services is concluded between the commission agent and the principal (the real owner of the goods). Therefore, the revenue received and remuneration must be reflected in the accounting of the commission agent. All payment received for intermediary activities creates its own turnover of funds for the commission agent.

The reflection of transactions in accounting is directly related to the participation of an intermediary in the relationship between the buyer and the seller, that is, he either participates in the transaction or acts only as a third party. Let's consider the algorithm of actions in both cases.

The commission agent takes part in the relationship:

- Proceeds from sales are first transferred to the commission agent's bank account or in cash directly to the cash desk.

- From the proceeds received, the commission agent retains remuneration for the provision of intermediary services.

- The amount remaining after deducting the remuneration is transferred to the principal's account.

The commission agent does not take part in the relationship:

- Proceeds from the sale of goods are usually transferred directly to the bank account of the consignor, the owner of the products.

- After the principal receives money from, he makes a transfer for intermediary services in favor of the commission agent.

Postings for the sale of goods in the accounting of the commission agent

| Account Dt | Kt account | Wiring Description | Transaction amount | A document base |

| 004 | Receipt of goods from the consignor | Purchase price | Packing list | |

| 004 | Shipment of goods to the buyer | Cost of goods | Packing list | |

| 44 | 02, 69, 76 | Reflection of expenses for the provision of intermediary services | Cost amount | Accounting certificate-calculation |

| 90.1 | Accrual of commission rewards | Reward amount | ||

| 68 | Calculation of VAT on transferred remuneration | VAT amount | Invoice, certificate of completion of work | |

| 90.02 | 44 | Write-off of commission agent's expenses when providing intermediary services | Amount of expenses | Accounting certificate-calculation |

| Crediting the amount of remuneration from the principal | Reward amount | Bank statement, payment order | ||

| 90.9 | 99 | Reflection of the financial result from | Net profit amount |

We reflect the commission sale of goods in the principal's accounting

When selling goods through a commission agent, the turnover of funds is generated by the principal, since only he is the owner of the valuables.

After sale, property rights pass to the buyer. It is then that the principal must display the proceeds received from the sale of goods by the commission agent at the sales price. This can only be done after submitting a report from the commission agent.

Postings for the committent

| Account Dt | Kt account | Wiring Description | Transaction amount | A document base |

| 45 | The goods are transferred for commission sales | Cost of goods | Packing list | |

| 90.01 | Reflection of the amount of proceeds from sales in the commission agent's report | Revenue amount | Commission agreement, accounting certificate-calculation | |

| 68 | VAT accrual on total turnover | VAT amount | Accounting certificate-calculation | |

| 90.02 | 45 | Write-off of actual cost for goods sold | Revenue amount | Invoice, certificate of completion of work |

| 44 | 76.5 | Commission services included in sales expenses | Cost amount | Invoice, certificate of completion of work |

| 19 | 76.5 | Allocation of the VAT amount from the cost of the commission agent's services | VAT amount | Invoice, accounting certificate-calculation |

| 76.5 | 62 | Adding intermediary services to the total costs of selling goods based on the commission agent’s report | Service amount | Invoice, certificate of completion of work |

| 68 | 19 | Acceptance of VAT amount for deduction from the budget | VAT amount | Accounting statement, sales book, invoice |

| 62 | Transfer of funds from the commission agent as income from the sale of goods, minus the requirement for remuneration | Revenue minus remuneration | Bank statement, payment order, invoice, certificate of completion of work | |

| 90.2 | 44 | Write-off of expenses for the sale of goods | Amount of expenses | Certificate of completion |

| 90.9 | 99 | Reflection of the financial result from the activities of the enterprise | Net profit amount | Accounting statement, Sales book |

How can selling goods under a commission agreement be beneficial? To whom and in what cases does it make sense to choose it? How to formalize a commission correctly and to the mutual satisfaction of the parties? How it is done commission trading scheme, if a commission agreement is concluded between organizations that apply different taxation regimes? We will answer these and other questions in our article.

It is convenient to trade consignment goods in the MyWarehouse service. In it you can accept goods for sale with a commission agreement, keep records of them, automatically generate a report to the consignor after the sale, look at profitability, and issue a return if the product is not sold. Register and try it now: it's free!

Advantages of trading under a commission agreementIf you are engaged in retail trade and have found a supplier who agrees to give you goods for sale under a commission agreement, you are in luck. And you’re especially lucky if you’re just starting out in business. The law allows money to be given for goods purchased under a commission agreement after it has been sold. That is, a commission trading scheme allows you to start working without large investments and without special risks.

If you produce a product or purchase it in large quantities for subsequent retail sale at different points, then a commission trading scheme can also be beneficial for you. At a minimum, this will increase the sales market. Some small store, located in a place where you yourself would not work, can quickly sell out goods that are not sold in your traditional outlets. At the same time, the store may not be able to buy a batch of such goods, but it will gladly accept it on commission.

The commission trading scheme is also beneficial because it makes it easier to process the return of goods than under a sales contract. If the product was purchased under the “purchase and sale” scheme, then in order to return it from the store back to the supplier, it is necessary to carry out a reverse sale. This creates problems in terms of taxation - when one of the parties to the transaction does not pay VAT, the second loses money because it cannot deduct VAT. If the delivery of goods is formalized under a commission agreement, this problem does not arise. The intermediary simply writes off the goods from off-balance sheet accounting and returns them to the supplier. However, when returning goods taken on consignment, there are some subtleties, and we will return to them in this material.

How commission trading is processed

In a simplified form, this diagram looks like this. The supplier (principal) gives his goods for sale to an intermediary (commission agent). In this case, the ownership of the goods does not pass to the latter. The commission agent sells the goods to the buyer, acting on his own behalf, but at the expense of the principal. As soon as the goods are sold, the principal ceases to be its owner. The commission agent reports to the supplier, gives him the proceeds for the goods and receives his remuneration.

So, how to arrange a commission correctly? Let’s say a certain company is going to sell a product to a store. First of all, the supplier and the store draw up a commission agreement, which states which of them is the commission agent, which is the principal, and also indicates that the first, on behalf of the second, will sell goods for a fee. It is also better to specify the amount of remuneration in the contract. This can be either a fixed amount for each product sold, or a certain percentage of sales. The law, namely Article 51 of the Civil Code of the Russian Federation, obliges the commission agent to report to the committent on sales. The deadlines for submitting the report are not regulated, but it is also better to write them down in advance. A commission agreement can be concluded for a specific period or be indefinite. Entrepreneurs themselves also decide whether to indicate the territory for its implementation. A sample commission agreement can be downloaded from our library of document forms.

The commission agreement has been concluded. What's next? Then the goods are transferred to the store, which is accompanied by an act of acceptance and transfer of goods for commission and a TORG-12 invoice. You can download a sample transfer and acceptance certificate, as well as an invoice, on our website. An act of acceptance and transfer of goods for commission is required if this is specified in the contract. If there is no such condition, then an invoice is sufficient.

The shipment of goods has arrived safely at the store, and the commission agent begins selling. By law, the sale of goods must begin no later than the next day after its acceptance. After a certain quantity has been sold, or the reporting period specified in the contract has passed, the store draws up a commission agent’s report. It states how many units of the product were sold, at what price and what the reward amount was. As we wrote above, it is better to stipulate the deadlines for submitting the report in the contract, although this is not required by law. You can agree to provide it every week or every month. We have a sample commissioner's report on our website.

In addition to the report, it is recommended to draw up and sign an agreement on the provision of services between the parties. After all, by making transactions on behalf of the principal, the commission agent provides him with a service. A document is being drawn up about this. The amount in the act is the amount of the commission agent's remuneration for the reporting period.

Along with the report, the intermediary transfers the proceeds to the supplier and retains his commission. Another option is also possible when the committent takes all the proceeds and only then transfers the remuneration to the commission agent. Then the cooperation continues or ends.

If the principal is not satisfied with the commission agent’s report in any way, he must report this within 30 days from the date of receipt of the document. However, this period can be changed with the help of a preliminary agreement of the parties.

Automation greatly simplifies the commission trading process. The MoySklad service offers the optimal solution for both the principal and the commission agent. In the system itself, you can create a commission agreement, take into account the shipment and acceptance of goods, record sales of commission goods, and automatically generate commission agent reports. At the same time, in all created forms and reports, revenue for goods sold, commission agent's remuneration, VAT and other necessary amounts are instantly calculated.

Now let's see what the law tells us about special cases.

Commission trading: special casesThe commission agent sold the goods more expensive or cheaper than expected

Let's say the goods were selling so well that the store decided to raise prices on them. In this case, the commission agent managed to obtain additional benefits, which, by law, he must equally share with the principal. Unless, of course, other conditions are provided for in the contract. And here you need to pay attention to one important detail regarding the processing and payment of this money. According to the letter of the Ministry of Finance of Russia dated June 5, 2008 No. 03-03-06/1/347, before part of the profit is paid to the commission agent, the committent must display this entire amount in income that is subject to income tax. And only after that accrue what is due to the commission agent.

If for some reason the goods were not sold at the agreed price, and the store reduced it, then there are two possible scenarios.

- The store proved to the consignor that it did not have the opportunity to sell the goods at a higher price, and this move prevented even greater losses. In this case, the commission agent will not be required to return the difference.

- The store failed to prove that the price reduction was a necessary step. Then, alas, the commission agent will have to compensate the supplier for the loss.

By the way, it is not forbidden to include these cases in the commission agreement. In addition, you can add conditions to it that, before changing prices, the commission agent must ask permission from the principal.

The contract was not fulfilled

Let's say that part of the goods that the principal delivered to the store turned out to be defective, or the agreed quantity of goods was not delivered, or for some other reason the commission agreement cannot be fulfilled due to the fault of the supplier. In this case, the law requires the principal to still pay the commission agent remuneration, as well as reimburse expenses. If the commission agreement cannot be executed due to the fault of the store, then, in turn, it will have to compensate the principal for damages.

Subcommission

Let's imagine that the store has found another profitable point of sale of goods, which is managed by another company. In this case, he has the right to conclude a subcommission agreement with this company. Then the commission agent is responsible for the actions of the sub-commission agent to his principal, and for the second store he himself becomes the principal. And a few important notes. Subcommission is possible unless otherwise specified in the commission agreement. In this case, the principal does not have the right to enter into relations with the subcommissioner, unless, again, otherwise provided by agreement of the parties.

The commission agent did not sell a single product during the reporting period

If all the goods remain in the warehouses and shelves of the store, the store has the right to return them to the consignor. The return of the goods, as well as its receipt, is issued with a TORG-12 invoice.

The trade management service MoySklad will help to significantly facilitate the process of returning goods from the commission agent to the consignor. The system has special forms in which returns are registered, and the entered data is automatically transferred to all reports that are related to the execution of the commission agreement.

Return of goods to the commission agent from the buyer

Let’s say that a retail buyer wants to return an item for some reason.

Considering that, when selling goods to a client, the commission agent, on his own behalf, entered into a sales contract with him, then he formalizes the refusal of this transaction.

If the buyer returns the goods due to detected defects, responsibility for them must be distributed between the commission agent and the consignor. If the goods were damaged due to the fault of the store, then the buyer will reimburse the costs. And if it turns out that the supplier is at fault, the commission agent will be entitled to reimbursement of expenses and remuneration.

The goods can be returned before the commission agent's report is signed by the parties, or after. In the first case, the intermediary makes an entry in the report for the amount of the return with a minus sign. In the second, the wholesale buyer, returning the goods, issues an invoice in the name of the commission agent. If the final buyer is a retailer, then he must write a statement to return the goods. After this, the commission agent returns the goods to the consignor, accompanied by a return note in his name, as well as an invoice. Based on these documents, the principal will be able to reduce his VAT payable.

Invoices for commission trading

Invoices for commission trade in retail

In our example, where the commission agent is a store, the latter does not issue invoices to customers, since in retail trade this document replaces a cash receipt with the VAT amount highlighted on a separate line. The principal also does not issue invoices to the commission agent. But at the same time, the store issues an invoice to the principal for the amount of its remuneration based on the results of the reporting period.

Our retail store selling under a commission agreement is not required by law to maintain an invoice log.

Indicators of CCP control tapes (only indicators, not the tapes themselves), as well as copies of the tapes, are transferred to the committent along with the commission agent's report, and the committent registers them in his sales book in order to charge VAT on the cost of goods sold.

Moreover, if a store, in addition to the principal’s goods, also sells its own goods, then accounting for these goods must be separate. With the help of the MySklad trading program you can easily fulfill this requirement. The program shows the commission agent how many of his own goods and how many of the goods received under the commission agreement. The principal sees in the system how much of his goods are on sale and by whom.

Invoices for wholesale commission trade

Now let's consider a situation where a commission agent sells goods in bulk on behalf of the principal, and both are VAT payers. In this case, invoices are mandatory accounting documents for them.

Since, under the terms of the agreement, the commission agent makes transactions with third parties on his own behalf, he also issues all invoices on his own behalf. The document number is assigned in accordance with the chronology of the commission agent. The invoice must be written in two copies. One must be handed over to the buyer, the second must be filed in the invoice journal. In this case, the invoice for the sale of consignment goods does not need to be registered in the sales book of the commission agent.

And the principal issues and enters in his sales book an invoice addressed to the commission agent, already numbered in accordance with his chronology. This document is not recorded in the intermediary's purchase book.

In this case, the indicators of the invoice that the commission agent issues to the buyer are reflected in the invoice, which is issued and recorded in its sales book by the supplier. The principal must also write out two copies - one to hand over to the commission agent, and the second to keep in his journal of registration of issued invoices.

The document received from the principal is filed by the commission agent in the journal of received invoices.

Based on the signed report and the corresponding act, the commission agent issues a separate invoice to the principal for the amount of his remuneration for the reporting period. This document is registered with the commission agent in the sales book, and with the committent - in the purchase book.

If the commission agent sells the supplier’s goods to the buyer at the same time as his own goods, then the buyer can be issued a single invoice for the specified goods.

More details about issuing invoices for commission trading can be found in the letter of the Ministry of Taxes and Taxes of Russia dated May 21, 2001 No. VG-6-03/404.

Commission agent on the simplified tax system - committent on the simplified tax system

If the commission agreement was concluded by companies, each of which applies the simplified tax regime (STS), then the commission agent, if questions arise about how to calculate taxes, must refer to Article 251 of the Tax Code of the Russian Federation. It directly states that when determining the tax base of a commission agent, property and funds received by him in connection with the fulfillment of obligations under a commission agreement are not taken into account as income. Income received to reimburse expenses incurred for the principal is also not taken into account. That is, only commission fees are considered income. Accordingly, revenue for goods sold is not counted as income. If the principal under the simplified tax system compensates the commission agent under the simplified tax system for any expenses, this money is also not subject to tax.

The date of receipt of income from the “simplified” intermediary is the date of receipt of remuneration from the principal into his account. If, under the terms of the contract, the commission agent withholds his remuneration from funds received from buyers, then the date of receipt of income is considered the day the money is received at the cash desk. It does not matter that the report may not have been signed yet, since advances are also included in the income of companies under the simplified tax system.

Expenses are recognized only after they are actually paid. Moreover, those expenses that are legally reimbursed by the principal (for example, for renting a warehouse where the goods are stored) are not considered expenses of the commission agent.

As for the principal, according to the letter of the Ministry of Finance No. 03-11-11/16941 dated May 15, 2013, his income is the entire amount received from the sale of goods, including commissions. Yes, in the scheme “commission agent on the simplified tax system - principal on the simplified tax system,” the remuneration paid by the principal, alas, cannot be attributed to his expenses, and tax will have to be paid on it. But! If the commission agent withholds his commission before transferring funds to the principal, the income will legally be equal to the amount that was actually received into the supplier's account. This means that if the committing company is on the simplified tax system, then it is better to specify exactly this option in the contract.

The day of receipt of income is the moment of receipt of funds to the current account or to the supplier's cash desk.

The principal under the simplified tax system is not obliged to issue an invoice for his goods, because The responsibility for drawing up this document rests only with the VAT payer.

Commission agent on the simplified tax system - principal on the OSNO

If the commission agent trades wholesale and is a “simplistic” agent, and the principal works on the general taxation system, then the intermediary will have to issue invoices. The fact is that in fact, the seller to third parties is the principal under OSNO, and not the commission agent under the simplified tax system, therefore the intermediary must calculate value added tax for the supplier and present an invoice to the buyer. The scheme is the same as what we wrote about above. The commission agent makes two copies of the document, one of which is issued to the buyer, and the second is filed in the journal of issued invoices, without registering it in the sales book. The indicators of these documents are reflected in the invoices that the committent issues to the commission agent and registers in his sales book.

And let us remind you that in retail trade, the invoice is replaced by a cash receipt with the VAT amount highlighted on a separate line.

The supplier reflects the received revenue based on the received report. Therefore, in the case where the commission agent is on the simplified tax system, and the principal is on the OSNO, it is important in the contract to reflect the procedure and timing of its provision. If it arrives later than the deadline, the supplier will still have to pay VAT on time.

The intermediary does not issue an invoice for the commission to the principal, since the commission agent's remuneration in the simplified form is not subject to VAT.

In the opposite situation, when the principal is on the simplified tax system, and the commission agent is on the OSNO, the intermediary should not issue an invoice to the buyers, because the seller is in fact the supplier, and he is exempt from VAT.

Commission trading is a form of sales of goods in which the transaction is concluded on behalf of an intermediary. The results of the completed transaction are sent directly to the previous owner of the item. The benefit of such cooperation for the intermediary is to receive a pre-agreed reward. Sometimes a specific amount is immediately set, sometimes a percentage of the price for which the object was sold is assigned.

Both you and us

Currently, organizing commission trade is a widespread practice in a variety of countries on our planet. The commission agents are usually those enterprises that have already been able to create a good reputation for themselves as reliable market participants. Principals who have not yet become famous among the public can, on fairly favorable terms, enter into a transaction for the sale or purchase of products, using the services of a commission agent.

There is wholesale and retail commission trade. The first option is most relevant for industrial enterprises. If a company has a warehouse surplus of a product and needs to quickly sell inventory, it is most convenient to enter into a transaction with such an intermediary. This option will be most profitable when selling a standardized product. An intermediary concluding wholesale transactions often additionally plays the role of a supplier for an industrial facility, since it is the easiest and most profitable for such legal entities to purchase goods used as industrial raw materials from agriculture.

I don't need that much

A consignment store may handle retail transactions. At such a point, you can equally purchase goods that you have already used and completely new products. Often, outlets sell raw materials produced in agriculture and finished products. The practice of cooperation according to this logic is widespread among cooperatives, markets, and collective farms. Individual private owners supply the product grown and produced by them, which is sold in an organized manner, for which the intermediary receives a certain percentage as a reward.

Work - only officially

To avoid misunderstandings and attempts to violate the established conditions, a commission trading agreement is concluded. All aspects of the relationship between the parties to the transaction will be subject to the document. The commission agent undertakes obligations for the transaction in accordance with the instructions of the principal. There is some remuneration for this. Several transactions may be mentioned in one agreement. These are carried out on behalf of the commission agent, but material support is the responsibility of the principal.

The rules for trading consignment goods require the fulfillment of all obligations assumed by the parties and declared by the signed agreement. The commission agent indicates that he plans to conclude the transaction on conditions that are most beneficial for the client. If it was possible to sell the product for an even higher price than was agreed upon by the principal, the profit in excess of what was planned should be divided between the parties to the transaction. If the parties are interested in another mechanism for distributing profits beyond what was previously predicted, this can be indicated when concluding an agreement in the documentation.

Everything is spelled out

In order for commission trading to satisfy the requirements and expectations of all interacting parties, at the stage of agreeing on the rules for concluding a transaction in relation to a product, they stipulate the time frame for the transaction to be carried out. You can specify specific dates or the number of days from the date of actual transfer of the product to the store, or you can even state that there is no deadline at all. Another option is to consciously refrain from mentioning this fact, which is equivalent to specifying the contract as unlimited.

The current rules of commission trading allow for an indication of exactly which site, territory, and address the transaction should be carried out. If this form suits everyone, the contract is concluded without mentioning this condition. The commission agent retains the right to conclude an additional agreement with a third party in order to transfer the product to him according to the logic of the subcommission. This is impossible if the primary agreement contains a ban on delegation of powers. When transferring obligations and products to the principal, all responsibility lies with the commission agent. It does not matter who carried out the operation - he or the subcommissioner. In relation to a third party, the commission agent turns into a principal with the ensuing obligations and rights.

Responsible approach

For commission trading to be successful, it is necessary to have all the goods intended for sale in the access area, preferably in the store. Therefore, it is important to think in advance about the availability and equipment of warehouses designed not only for the long-term storage of sufficiently large volumes of products, but also designed in such a way that it is convenient to accept and ship items, sell, and, if necessary, process. This format for selling goods assumes that the commission agent is responsible for the entire accepted product and must take care of it and store it in the conditions required for a specific item.

The rules of commission trading of the Russian Federation allow for lending to a client and the provision of additional services, but strictly under the responsibility of the commission agent. The store can provide services in the form of regular transmission of information, market information, help conclude contracts with transport companies and assist customers in other ways.

Which one is more convenient for you?

It is easiest to keep track of goods in commission trade, when all the products are in front of the commission agent, but in each individual case you can agree with the consignor in such a way that the items will be directly shipped to the client from the warehouse of the primary supplier. Recently, this practice has become more and more widely used, since the accounting operation is carried out through electronic systems. Constantly collaborating enterprises can create a common database, which makes the calculation process much simpler and the likelihood of errors is reduced to a minimum. On the other hand, a customer purchasing multiple items from different consignors may be frustrated by having to receive different products at different addresses.

It is most profitable to organize commission trade through a consignor's warehouse, when the store provides commission services in relation to large products, goods that require large space for placement or expensive equipment to ensure adequate storage conditions. Often the situation develops in such a way that only the provision of conditions at a price is comparable or exceeds the benefit from the transactions, so the commission agent cooperates with the principal, using his warehouse capabilities.

What about the money?

According to the rules of commission trading, already at the stage of concluding an agreement between the supplier and the commission agent, it is necessary to decide how the remuneration will be calculated, how it should be transferred, and in what form the financial amounts should be transferred. A whole range of important factors play a role, the most significant of which is the variety of products intended for sale.

As can be seen from world practice, trading on commission goods with the lowest percentage of profit for the commission agent is the sale of a simple, homogeneous product that does not have technically complex elements or structures. This includes raw materials. If the product is in the complex category, you can expect to earn decent commissions, but the transaction costs will be higher. In any of the options, there is a chance that the commission agreement will not be fulfilled for reasons that the principal cannot influence. In such a situation, the commission agent retains the right to receive remuneration and compensation for expenses associated with the agreement.

Current approach

Recently, the rules of commission trade in non-food products have received the greatest interest, since this particular area of products is especially in great demand among the general population. From the current regulations established at the federal level, it follows that according to this logic, it is possible to sell not only new products, but also those that have already been used before. The main condition is a sufficient level of quality, that is, the product must be suitable for further use for its intended purpose. We accept only items that do not require repair or restoration. All products must meet hygienic standards, sanitary conditions, safety requirements regarding the health and life of the end user. You cannot refuse acceptance solely on the basis of wear and tear of a product, if it is still suitable for use for its main purpose.

The law does not allow such trade in consignment goods, the object of which is items prohibited for free distribution, as well as items withdrawn from circulation from ordinary citizens. It is necessary to take into account all legal regulations that are relevant at the present time.

About restrictions

When trading on commission, the following information should be taken into account: in no case should you take weapons (service, military) from an interested client for its further sale. The restriction also applies to special uniforms, equipment designed for the army, and other military products.

If the consignor offers gas equipment for sale, it can be accepted only if there is documentation confirming the completion of the inspection procedure. Certificates must be issued exclusively by specialized services responsible for the gas industry.

Expensive and rich

When organizing commission trade, you must also take into account the fact that it is prohibited to sell animal skins through this format if they do not bear the manufacturer’s mark, as well as various items related to jewelry. These are unprocessed stones, certified precious metal bars and products made from precious metals, not sealed with a stamp. Products made from precious metals, precious stones, amber, and bog oak cannot be accepted from legal entities. The law prohibits the sale through thrift stores of processed, cut precious stones that are not fixed in any product, as well as medals, orders, tokens, and signs made from precious metals.

Current laws establish restrictions on cooperation with principals trying to present for sale through a consignment store products, medicines and underwear intended for medical use, stamped by any enterprise or other legal entity.

Safety first

All legal types of commission trade in our country require the acceptance from interested parties only of goods that do not pose a danger to the potential buyer. This imposes restrictions on some categories of non-grocery products. For example, you cannot bring to the store underwear and clothing intended for children from birth to preschool age, as well as toys made for children three years of age or younger. The only exceptions are items packed in hermetically sealed protection.

It is prohibited to accept vehicles for sale from the public if they are accompanied by false documentation purporting to confirm registration. Similar restrictions apply to transport, a visual inspection of which gives reason to suspect a change in individual numbers. If the goods were brought by a minor citizen aged 8-15 years, items can be taken from him only with the official consent of a guardian, parent, or adoptive parent.

Everything is official

In order to correctly accept a product from a private person, the representative of the consignment store must require the presentation of a passport or other form of document proving the identity of the applicant. If a legal entity is interested in concluding a transaction, it is necessary to check the correctness of the representative’s power of attorney and a complete list of invoices. Documents must be filled out correctly and issued in accordance with current federal office procedures.

If the product is presented by the primary seller as new, the representative of the consignment store is obliged to check the availability of certificates for it, as well as clarify the fact of successful completion of the mandatory certification declared by law. The principal's area of responsibility is to provide accompanying documentation proving safety and compliance with accepted standards.

Financial aspects

The current legislation establishes taxation of commission trade as UTII. This is due to the fact that this type of transaction belongs to retail trade. In order to calculate the amount of taxes due for payment correctly, the store’s accounting department must keep records, recording in it all the amounts of products accepted for sale and sold. To eliminate possible discrepancies, it is necessary to conclude an agreement with each consignor, indicating in it all the items intended for sale, as well as the conditions under which the store can enter into a transaction with an interested buyer.

Often one consignor provides a retail outlet with many items for sale at once. The best option for documenting such cooperation is a standard agreement, supplemented by an annex with a complete list of accepted products. The process of concluding an agreement is accompanied by the issuance of labels.

Everything is for a reason

By signing the sales agreement, the principal and the commission agent must come to an agreement regarding the value of the goods. Already at the stage of signing the agreement, the store representative must inform the client how great the supply and demand for the items presented by him is. This allows the consignor to determine the most favorable price for the product. The remuneration received by the point of sale is usually determined as a percentage of the price at which the item was sold.

Additionally, the agreement immediately stipulates the conditions for reducing the price and the timing of such an operation. For one item, markdowns are possible no more than three times. In a separate case, the commission agent may agree to continue trying to sell, lowering the price further, but the classic option for cooperation is returning the product to the principal after the third markdown. In such a situation, the client must reimburse the seller for the costs associated with storing the name in the store. These amounts are negotiated at the stage of concluding the agreement.

What to do?

If the store is interested in the product presented and it does not violate the current legislation, after concluding an agreement between the principal and the commission agent and observing all the formalities of the procedure, you can proceed directly to the sales process. On the day of reception or the next day, the commission agent is already obliged to display the received product in the hall where the product is available for viewing by potential buyers.

The responsibility of the commission agent is the compliance of the declared characteristics and the actual condition of the product. To avoid misunderstandings, the current condition is assessed at the time the products are received from the consignor. A client who has chosen a product for himself in a consignment store does not have the right to return it. As an exception, new products are found to have manufacturing defects that were not identified at the stage of accepting the product for sale from the consignor. The buyer has only two days to return the item to the store with evidence of his innocence. The principal receives the amounts corresponding to those agreed upon in the transaction on or before the third day from the date of sale. Money is issued only if the interested person has official identification documentation and an agreement signed by the seller and the store representative.

Historical summary

Commission trading was most active during the USSR period. Numerous locations throughout the country accepted manufactured goods to effectively serve the population: some had unwanted items, others needed them, and some were simply collecting random purchases. Consignment retail outlets were of particular interest given the lack of variety of products in regular stores. To this day, some say that Soviet second-hand stores are not just a business of that time, but an expression of an entire era through the prism of social life.

To control operations, a system of rules was created to regulate the functioning of thrift stores. At such sales points it was possible to purchase not only used household items, but also completely new goods. The State Trade Inspectorate closely monitored the work of retail outlets. Already at that moment it was forbidden to sell items if they were considered withdrawn from the circulation of citizens. It was unacceptable to sell materials for construction, production, equipment, and machines through commission points.

The rules of commission trade in non-food products regulate the relationship between the commission agent and the principal under a commission agreement, as well as the commission agent and the buyer when selling non-food products accepted on commission.

A commission agent is understood as an organization, regardless of its legal form, as well as

visual entrepreneur carrying out prod. goods accepted on commission under a purchase and sale agreement, under the principal - a citizen, the goods on commission for the purpose of Selling it by the commission agent for a fee, and under the buyer - a citizen who intends to purchase or who is purchasing using goods exclusively for personal needs not related to making a profit.

Goods for commission are accepted from citizens of the Federation, foreign citizens, and stateless persons.

Until the moment of sale (transfer) to the buyer of the goods accepted for commission, the ownership of it remains with the consignor. The commission agent is responsible to the principal for the loss, shortage or damage of goods in his possession transferred for sale.

New and used non-food products are accepted for commission.

Acceptance of goods is formalized by a commission agreement, receipt, invoice or other document, the type of which is determined by the commission agent independently. The specified document is drawn up in two copies (one for each party) and signed by the commission agent and the principal.

Acceptance for commission and sale of antiques are carried out in accordance with the Rules and in compliance with the requirements of the legislation of the Russian Federation regulating the procedure for the sale of antiques.

Products made of precious metals and precious stones are accepted for commission in accordance with the requirements for them, stipulated by the Rules for the sale of certain types of goods.

Admission to the commission and the sale of civilian weapons are carried out in accordance with the requirements of the Federal Law “On Weapons”, as well as other regulatory legal acts of the Russian Federation regulating the circulation of civilian weapons and ammunition in Russia.

Gas stoves and cylinders for them are accepted for commission if there is a document confirming their suitability for intended use, issued by the relevant gas services*

The commission does not accept goods that, in accordance with the legislation of the Russian Federation, are withdrawn from circulation, the retail sale of which is prohibited or limited, as well as goods that cannot be returned or exchanged for a similar product of a different size or shape. size, style, color or configuration.

A product label is attached to a product accepted for consignment, and for small items a price tag is attached indicating the document number issued upon acceptance of the product and the price.

The list of goods and the product label must contain information > characterizing the condition of the product (new, used, degree of wear, main product features, defects of the product)

The list of goods accepted for commission and the product label are signed by the commission agent and the consignor.

Goods for commission are accepted from citizens upon presentation of a passport or other identification document

The price of the goods accepted for commission and the amount of commission that the principal is obliged to pay to the commission agent are determined by agreement of the parties.

An item accepted for commission must go on sale no later than the next day after its acceptance, excluding weekends and holidays.

If there is a delay in the receipt of goods for sale due to the fault of the commission agent, he must pay the principal a penalty in the amount of three percent of the remuneration amount for each day of delay. By agreement of the parties, a higher amount of the penalty may be established.

If, before sale to the buyer, defects are identified in a new product that were not discovered when it was accepted for commission, then such goods are removed from sale * It is returned to the consignor, unless it is proven that the defects arose through the fault of the commission agent, without paying the commission agent’s expenses for storing the goods.

When selling a product whose warranty period has not expired, the buyer must be given a warranty card received from the consignor, a technical passport, a service book or another document replacing it, confirming the buyer’s right to use the remaining warranty period

It should be noted that the buyer’s demands for replacement of goods of inadequate quality with goods of a similar brand (model, article), for free elimination of defects in the goods and for reimbursement of expenses for their elimination are subject to satisfaction with the consent of the commission agent.

Instead of presenting all of the above requirements, the buyer has the right to refuse the purchased goods and demand a refund of the amount of money paid for it. In this case, the goods of inadequate quality must be returned to the commission agent at his request at his own expense.

The procedure and amount of markdown of goods accepted for commission are agreed upon by the commission agent and the committent when concluding a commission agreement. It also determines the method of notifying the principal of the summons and the timing of his appearance.

If the principal refuses the markdown, the goods are returned to him* In this case, the contract may provide for reimbursement of expenses for storing the goods.

In cases where the commission agent has completed a transaction on terms more favorable than those specified by the principal, the additional benefit is divided equally between the parties, unless otherwise provided by agreement between them.

Money for the sold goods is paid by the commission agent to the principal no later than the third day after the sale of the goods.

Payment of money, as well as the return of goods accepted for commission but unsold, are made upon presentation by the committent of a document confirming the conclusion of the commission agreement, a passport or other document identifying the committent.

Where to start your business - a step-by-step plan from scratch for beginners Where to start a business

How to really make good money on the Internet without investments

Homemade handmade dumplings as a business

The best and unusual business ideas from around the world Business proposals for small businesses

IML delivery service delivery points